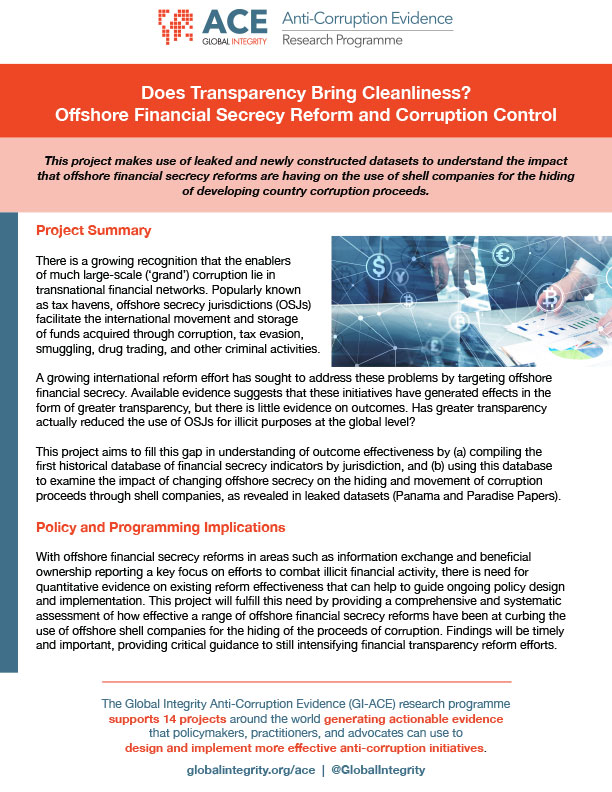

Does transparency bring cleanliness? Offshore financial secrecy reform and corruption control

This project makes use of leaked and newly constructed datasets to understand the impact that offshore financial secrecy reforms are having on the use of shell companies for the hiding of developing country corruption proceeds.

Click here for the Project One-Pager

To learn more about this project, contact Principal Investigator Daniel Haberly

Project Summary

There is a growing recognition that the enablers of much large-scale (‘grand’) corruption lie in transnational financial networks. Popularly known as tax havens, offshore secrecy jurisdictions (OSJs) facilitate the international movement and storage of funds acquired through corruption, tax evasion, smuggling, drug trading, and other criminal activities.

A growing international reform effort has sought to address these problems by targeting offshore financial secrecy. Available evidence suggests that these initiatives have generated effects in the form of greater transparency, but there is little evidence on outcomes. Has greater transparency actually reduced the use of OSJs for illicit purposes at the global level?

This project aims to fill this gap in understanding of outcome effectiveness by (a) compiling the first historical database of financial secrecy indicators by jurisdiction, and (b) using this database to examine the impact of changing offshore secrecy on the hiding and movement of corruption proceeds through shell companies, as revealed in leaked datasets (Panama and Paradise Papers).

Policy and Programming Implications

With offshore financial secrecy reforms in areas such as information exchange and beneficial ownership reporting a key focus on efforts to combat illicit financial activity, there is need for quantitative evidence on existing reform effectiveness that can help to guide ongoing policy design and implementation. This project will fulfill this need by providing a comprehensive and systematic assessment of how effective a range of offshore financial secrecy reforms have been at curbing the use of offshore shell companies for the hiding of the proceeds of corruption. Findings will be timely and important, providing critical guidance to still intensifying financial transparency reform efforts.

Research Question

What effects are initiatives to increase the transparency of offshore secrecy jurisdictions having on the use of these jurisdictions for the hiding of developing country corruption proceeds?

Methodology

The main challenges in our area of study are related to data availability, and our methodology is designed to directly address these challenges. Firstly, we are drawing on the expertise of the Tax Justice Network to construct the first historical database of changing financial secrecy indicators in key jurisdictions. Secondly, we are exploiting the window that new leaked datasets (the Panama Papers, Paradise Papers, and Offshore Leaks) provide into the use of shell companies by developing country elites, including for illicit purposes such as the movement and storage of the proceeds of corruption. Putting these together will allow us to conduct comprehensive statistical analyses of how the changing international financial secrecy regulatory and enforcement landscape has impacted the international landscape of illicit shell company use.

Research Team Members

- Daniel Haberly, Senior Lecturer in Human Geography, University of Sussex School of Global Studies, Centre for the Study of Corruption and Centre for Global Political Economy

- Alex Cobham, Chief Executive, Tax Justice Network, and Visiting Fellow, Kings College London

- Valentina Gullo, Research Fellow, University of Sussex School of Global Studies and Centre for the Study of Corruption

Publications

Related Blog Posts

Why do people set up offshore shell companies? Some preliminary findings from the Panama and Paradise Papers

GI ACE researcher Dan Haberly analyses the structure behind offshore shell company…

Mapping Politically Exposed Person (PEP)-linked shell companies in the Panama and Paradise Papers

GI ACE researcher Dan Haberly analyses the changing international regulatory landscape has…

A new map of financial transparency reform: 2000-2015

GI-ACE researcher Daniel Haberly’s first project workshop, “Dark Architectures: Advancing Research on…

Does transparency bring cleanliness? Offshore financial secrecy reform and corruption control

Researcher Dan Haberly discusses GI-ACE project attempting to understand how years of…